- "Sales growth: Sales are the life-blood of a company. If sales are drying up, that puts added pressure on profits and cash flows and thus the dividend, too.

- Interest coverage (EBIT/interest expense): If a company is having trouble paying the interest on its debt, there's a greater chance that its creditors will get worried and raise the company's cost of borrowing, which could reduce net income. In a worst-case scenario, the dividend could be cut to accelerate the repayment of principal.

- Net debt/EBITDA: This is a common measure ((Debt-Cash)/EBITDA) that creditors and ratings agencies use to determine credit quality and it's commonly used as a metric in debt covenants. A firm that has borrowed too much or is struggling to pay down its debt relative to its profitability is more likely to have a risky dividend.

- Dividend growth rate: A slowing dividend growth rate could be a sign that the company is less confident in its future growth potential. Eventually, all companies' dividend growth rates decline, but you want to see a steady decrease over many years and not a sharp drop.

- Earnings cover: Even though I don't think it's the best measure of dividend health, earnings cover (Net Income/Dividends Paid) remains the most common metric cited by both companies and investors alike, so it should be considered in any dividend analysis.

- Free cash flow cover: Free cash flow cover ((CFO-CapEx)/Dividends Paid) is a better measure of dividend health than earnings cover because companies don't pay out earnings -- they pay out cash. As such, I'd rather look at a company's cash flows than net income.

- Operating margin: A company whose margins are contracting could be facing increased competitive pressures or becoming less efficient. When this occurs, less money falls to the bottom line and to cash flows and the dividend can become riskier. Cyclical companies' margins will naturally ebb and flow. In those cases, use rolling 5-year margins to account for the business cycle.

- Return on equity: Companies that are unable to sustainably generate returns above their cost of equity are likely destroying shareholder value and usually have lower growth potential. Neither are good things from a dividend perspective."

I have found this a very handy tool to slice and dice a company's dividend related data. For one thing, it s a good reminder to look at coverage from multiple perspectives. Dividend Compass weights FCF cover as 25% of its rating.

The Dividend Compass ranks stocks using this rating system

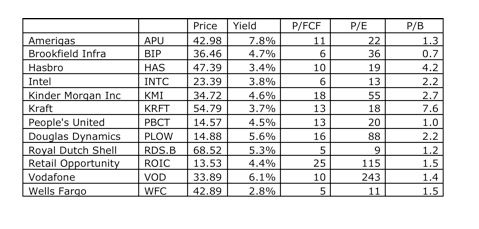

I put Royal Dutch Shell (RDS.B) through the Dividend Compass to get a closer look at the health of its dividend. The results were mixed

Royal Dutch Shell scores well on earnings and revenue related metrics but its Free Cash Flow is pretty mixed. The other negative factor which is pretty easy to spot is anemic dividend growth. You can see the data input below that generate the scores above.

All in all Dividend Compass is a valuable analytical tool. It incorporates most of the key objective data and presents it in a way that helpful to do a quick first pass to get a feel for the company's viability for a dividend investor. The weightings and rankings are subjective, people can have different opinions on them, but they strike me as roughly right. Especially the focus of Free Cash Flow. Notice that yield which is most everyone's first thought in dividend investing does not count for much. Thus, Royal Dutch Shell does not get all that much credit from the Dividend Compass for its 5.3% yield.

Dividend Compass is not a substitute for in depth research. It does provide a profile sketch of the company, in about five minutes of analysis, a picture of Royal Dutch Shell emerges - well managed earnings, good not great on margins and ROE, poor dividend coverage and oscillating FCF cover. It requires more investigation to get beyond these numbers but like all good analytical tools Dividend Compass leads you to the next level of interesting questions to ask.